Market snapshot for tokenized real estate 2026

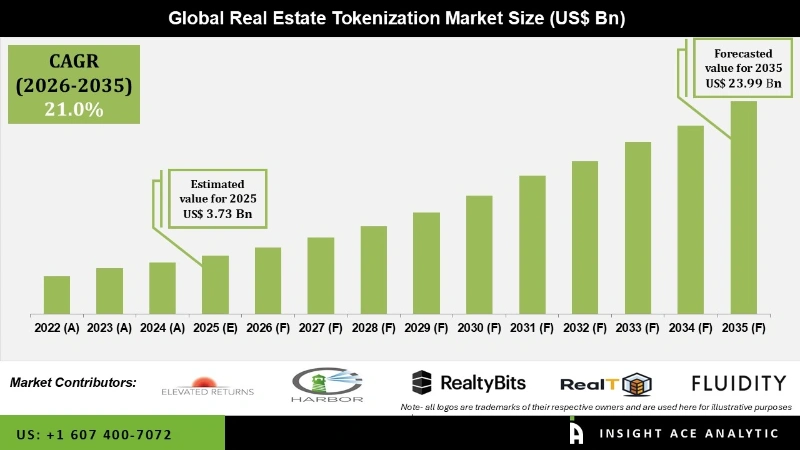

The promise of tokenized real estate is often measured in trillions, but the current reality is measured in fractions. While industry forecasts suggest the global market for tokenized real estate could reach $3 trillion by 2030, representing 15% of total real estate assets under management, the actual adoption curve remains shallow. Today, tokenized real estate accounts for far less than 0.1% of the roughly $300 trillion global property market, highlighting a significant gap between projected growth and current execution.

Despite this modest market share, investor sentiment is shifting. Institutional investors and high-net-worth individuals are increasingly viewing real estate as a primary target for tokenization. Recent data indicates that by 2026, institutional investors expect to allocate 5.6% of their portfolios to tokenized assets, while high-net-worth individuals plan to allocate 8.6%. Real estate itself is cited as the second most attractive tokenized asset class by both groups, trailing only behind traditional equities or stablecoins in some surveys.

This divergence between massive potential and slow uptake defines the 2026 landscape. The technology has matured enough to offer fractional ownership and improved liquidity, yet regulatory fragmentation and platform fragmentation continue to limit scale. For investors, this means the market is no longer experimental, but it is far from mainstream. The focus has shifted from proving the concept to solving the distribution and compliance challenges that prevent wider adoption.

The trajectory of this asset class is closely tied to broader digital asset trends. As traditional finance integrates blockchain infrastructure, the correlation between tokenized real estate performance and broader crypto or fintech ETFs becomes more pronounced. Understanding these macro trends is essential for evaluating the viability of specific platforms and the underlying assets they tokenize.

Regulatory shifts shaping the 2026 landscape

The regulatory environment for tokenized real estate has moved from experimental gray zones to defined frameworks in 2026. This shift is driven by three major pillars: the EU’s Markets in Crypto-Assets (MiCA) regulation, the ongoing application of MiFID II, and evolving guidance from the U.S. Securities and Exchange Commission (SEC). These rules determine whether tokenized properties are treated as standard securities or specialized digital assets.

In Europe, MiCA provides a unified license for crypto-asset service providers, but tokenized real estate often falls under the broader MiFID II umbrella. This means platforms must comply with strict investor protection and transparency rules typical of traditional financial markets. The European Securities and Markets Authority (ESMA) has clarified that real estate tokens representing ownership shares are financial instruments, requiring full compliance with existing securities laws rather than relying on crypto-specific exemptions.

The United States continues to rely on the Howey Test to determine if a token is a security. While the SEC has not issued specific real estate tokenization rules, enforcement actions against unregistered offerings have pushed platforms toward Reg D, Reg S, or Reg A+ exemptions. This creates a fragmented landscape where U.S. platforms often restrict access to accredited investors, limiting the liquidity advantages that tokenization promises.

Asia presents a different model. Hong Kong’s Securities and Futures Commission (SFC) has approved specific tokenized real estate platforms under its new licensing regime, treating them as regulated securities offerings. This approach allows for broader retail participation under strict custody and disclosure rules, positioning Hong Kong as a leader in institutional-grade tokenization.

| Region | Primary Framework | Investor Access | Key Constraint |

|---|---|---|---|

| EU | MiCA + MiFID II | Broad (with KYC) | Full securities compliance |

| US | SEC Howey Test | Accredited only | Registration exemptions |

| Asia (HK) | SFC Licensing | Broad (regulated) | Platform licensing |

The divergence in regulatory approaches creates arbitrage opportunities but also compliance complexity. Platforms operating globally must navigate these overlapping frameworks, often requiring separate legal structures for EU and U.S. investors. As 2026 progresses, harmonization efforts between the EU and U.S. may reduce these barriers, but for now, jurisdictional compliance remains the primary hurdle for scaling tokenized real estate.

Top platforms for fractional property ownership

The market for tokenized real estate has matured from experimental pilots to established platforms with clear operational models. By 2026, institutional investors expect to allocate 5.6% and HNW individuals 8.6% of their portfolios to tokenized assets, with real estate cited as the second most attractive option for both groups [[src-serp-6]]. This shift demands platforms that offer more than just token issuance; they require robust secondary markets, legal compliance, and transparent property management.

The following comparison outlines the leading platforms currently facilitating fractional property ownership. These platforms differ significantly in their target investor base, minimum entry points, and liquidity mechanisms. Propy focuses on cross-border transactions and closing infrastructure, while RealT emphasizes accessible, low-cost entry into US rental properties with daily liquidity.

| Platform | Min. Investment | Property Type | Liquidity | Region |

|---|---|---|---|---|

| RealT | $50 | Residential Rentals | Daily (Secondary Market) | US (Multi-state) |

| Propy | Varies | Commercial & Residential | Low (OTC/Listing) | Global |

| Lofty AI | $10 | US Residential | Daily (Secondary Market) | US (Florida/Texas) |

| Realwise | €50 | European Commercial | Quarterly/Annual | Europe (Luxembourg) |

RealT and Lofty AI lead the charge in democratizing access, allowing investors to start with as little as $10 to $50. These platforms primarily tokenize US residential rental properties, leveraging blockchain to streamline ownership records and distribute rental yields automatically. Their secondary markets allow investors to sell tokens daily, providing a level of liquidity unmatched by traditional real estate.

Propy distinguishes itself by focusing on the closing process itself, using blockchain to verify titles and manage transactions across borders. While its liquidity is lower, its infrastructure is critical for high-value commercial and residential deals that require complex legal verification. Realwise targets the European market, offering tokenized commercial real estate that appeals to investors seeking exposure to EU property markets with stricter regulatory oversight.

When choosing a platform, consider the jurisdiction of the underlying property. US-based platforms like RealT and Lofty AI benefit from clear SEC guidelines for security tokens, while European platforms like Realwise operate under MiCA regulations. Always verify the platform’s legal structure and how it handles property management, as token ownership does not equate to direct property control.

Liquidity and secondary market realities

Liquidity in tokenized real estate is often overstated. While platforms advertise "daily" trading, actual volume is frequently thin, and selling tokens can take days or weeks depending on market depth. Investors must distinguish between the ability to list a token and the ability to execute a trade at a fair price. Secondary markets are primarily driven by institutional flows and high-net-worth participants, meaning retail investors may face significant slippage or inability to exit positions during market stress.

In addition, the "liquidity premium" is often offset by higher fees and lower yields compared to direct ownership or REITs. Investors should view tokenized real estate as a long-term hold rather than a liquid cash substitute. The primary value proposition remains fractional access and automated distribution, not immediate tradability.

Frequently asked questions about tokenized real estate

Is real estate going to be tokenized?

Adoption is accelerating among institutional investors, who expect to allocate 5.6% of their portfolios to tokenized assets by 2026. High-net-worth individuals plan to allocate 8.6%. Real estate is currently the second most attractive tokenized asset class, trailing only digital securities, indicating strong institutional interest despite slower retail adoption.

What is the projected market size for tokenized real estate?

Research from ScienceSoft predicts the global market for tokenized real estate will reach $3 trillion by 2030, representing approximately 15% of total real estate assets under management. This growth is driven by increased liquidity and fractional ownership capabilities, though current market share remains below 0.1%.

How does tokenization compare to traditional real estate investing?

Tokenization enhances liquidity and lowers entry barriers. Unlike traditional real estate, which requires large capital outlays and involves lengthy transaction processes, tokenized shares can be traded on secondary markets. This allows investors to diversify across multiple properties with smaller amounts of capital, though regulatory frameworks remain in development and secondary market depth is often limited.

No comments yet. Be the first to share your thoughts!